From DataAlways

We ended last year’s edition by emphasizing the diverging paths of the two largest cryptoassets: Bitcoin needed to find a way to monetize its blockspace and Ethereum needed to focus on scaling by pushing users onto L2s. In 2023, we saw encouraging signs of both.

Bitcoin

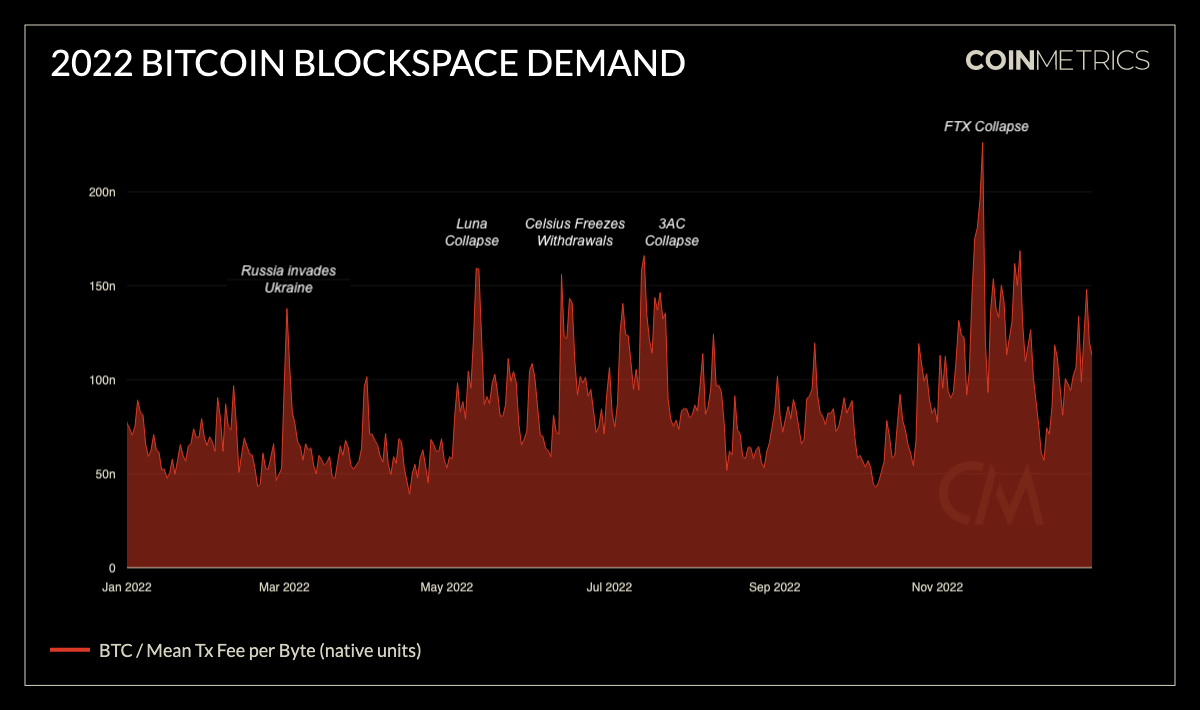

Despite a historically small bear market, the Bitcoin network began the year in its longest modern drought of blockspace demand. The only strong drivers of fee surges in 2022 were panics brought on by institutional failures.

The pandemic brought crypto into mainstream discussions and gave birth to a new breed of bitcoiner—those who are only concerned with the monetary properties of the system and put the asset above the network. This class of bitcoin holder rarely, if ever, transacts on the chain.

Only a year later and empty blockspace now appears to be a relic of the past; Bitcoin finds itself in its longest ever period of saturated blockspace.

Source: Dune Analytics - Bitcoin Block Fullness

This year saw the rise of inscriptions, much to the displeasure of the pandemic class of bitcoiners. Being newcomers to the ecosystem, these people lack a fundamental understanding of the difference between Bitcoin the network and bitcoin the asset. The Bitcoin network is designed to facilitate trustless transactions tracked in a global ledger. The asset is an incentivization scheme to encourage miners to populate the ledger.

Without trustless and permissionless transactions there is no reason for the ledger or the asset to exist. Any attempt to restrict what types of data can be written goes against the very nature of the blockchain. At its core Bitcoin is an immutable data layer.

The crowning delusion of the anti-inscription crowd is that JPEGs are using up all the space on the blockchain and making it impractical for people to transact on the chain, but it’s clear from the data that this isn’t the case. Canonical inscriptions (images, videos, text, etc.) did take the network by storm in February, but by the end of April the hype had largely faded and now only account for a couple percent of blockspace.

Source: Dune Analytics - Bitcoin Blockspace Usage by Transaction Type

The overwhelming majority of inscriptions today relate to BRC-20s: a novel but inefficient token standard, where data is encoded in JSON envelopes to enable altcoin transactions on Bitcoin. The BRC-20 protocol was birthed when Ordinals demonstrated to the mass market the non-fungibility of bitcoins (and they do leverage inscription explorers out of convenience), but they benefit significantly less from the Segwit discount, and could easily be adapted if inscriptions were blocked today.

Further, when we filter out inscriptions and BRC-20 transactions, we see that traditional bitcoin transaction counts remain in line with pre-inscription values. There are just as many legitimate bitcoin transactions today as there has been in the past. While Bitcoin maximalists attribute the symptom of high fees to the origin, the deeper cause is the influx of users and the renewed interest in the ecosystem.

Despite being the largest cryptoasset, Bitcoin was frequently ridiculed for its limited activity. Both Tron and Binance Smart Chain generated more fees than Bitcoin in 2022. Through the first ten months of this year, Bitcoin again trailed Tron in annual fee revenue, but the dynamic shifted suddenly when Binance listed its first BRC-20 token.

Bitcoin instantly entered a period of fee mania and surpassed Ethereum in single-day fees paid for the first time since 2020. By the end of the year the Bitcoin vs Tron fee comparison wasn’t even close.

Source: Coin Metrics (BTC) and Tronscan(TRX)

Ethereum

Despite the renaissance year for Bitcoin, Ethereum remained the king of demand with no meaningful challengers. The most significant decline was seen by Binance Smart Chain, experiencing a 65% collapse in fees and dropping from second to fourth place.

Surges of inscriptions on Avalanche caused the asset to leapfrog Solana (which showed strong non-inscription blockspace demand to end the year), and find parity with Ethereum’s top rollups.

Source: DefiLlama

The essential Ethereum statistic of the year was the growth in gas usage by Ethereum L2s amid a continued lack of demand for base asset transfers. With Ethereum pivoting to a rollup-centric scaling model, the dream of cheap transfers on mainnet is dead. If the asset succeeds in the long-term, the majority of users will be relegated to L2s and seldom touch the main chain.

Source: Dune Analytics - L2 Data (@funnyking), Transfers(@data_always)

Isolating the L2 data reveals that the growth in total gas usage has been fueled by increasing competition. In the early part of the year, Arbitrum and Optimism accounted for 80% of gas usage. Although their gas usage has continued to rise, their combined market share has now dropped to 20-30%. The current scaling landscape is considerably more diverse, featuring alternatives such as Base, ZkSync Era, StarkNet, and Linea, each optimized for specific use cases.

Source: Dune Analytics - Ethereum L1 Gas Usage by Various L2s

In addition to the growth from L2s, this year saw a large resurgence in gas used by DeFi. In 2022, NFTs had surpassed decentralized exchanges as the most significant gas user. However, with retail interest waning and NFT demand reaching its lowest level since 2021, DeFi experienced a boom. The latest trend: Telegram trading bots. While the return of NFT demand remains uncertain for now, decentralized exchanges reign supreme and dominate the narrative landscape.

Source: Dune Analytics - ETH Transfers, NFTs, DEXs, L2 Call Data

However, the DEX landscape has undergone a dramatic transformation over the past two years. A new challenger has emerged: despite its smaller market cap, DEX volume on Solana is now comparable to Ethereum.

As Ethereum continues to push users away from the main chain, the battle will be fought between alt-L1s and Ethereum L2s. When we consider the current centralized state of L2s, it’s not clear that users are better off staying in the Ethereum ecosystem in the short term.

The Coming Year

The big story for Ethereum blockspace in 2024 will be EIP-4844. Set tentatively for Q1, the upgrade is a redesign of the call data marketplace and provides an alternate avenue for L2s to write data to the main chain. The objective is to establish a clear delineation between mainnet use cases and L2s, thereby stabilizing the costs associated with scaling solutions during events like airdrops and NFT mints.

Researchers originally believed that this alternate gas market, known as blobspace, would initially be underutilized. However, given the recent surge in inscription spam across EVM chains, this assumption no longer holds. Blobspace will quickly be filled by economically rational transactions.

Inscriptions served as a proof of concept, demonstrating that Bitcoin has the potential to evolve into an unstoppable data layer. Looking ahead, the key problem is determining the most sensible data to publish to the blockchain. In our view, the most promising option is rollups, which offer the potential to scale Bitcoin with better user experience than the Lightning Network. Posting this kind of data to the blockchain often becomes conflated with Ordinals, but these applications would be better served by customizing the data embedding techniques to optimize their own use cases and by adopting their own unique protocol identifiers.

This year should also see the launch of Runes, an alternative standard for tokens Bitcoin that aims to displace BRC-20s. Will the community embrace the technically better option or do BRC-20s have too much memetic momentum to overcome? We expect speculators to keep chasing the newest hot ball of money and for Runes to thrive, but too much money has been made on BRC-20s and they are too popular in Asia to go away any time soon.

Is this the year that Drivechains finally gain traction? While we are optimistic, the Bitcoin community is still reeling from the impact of Taproot and remains too shell-shocked to adopt major changes. We don’t expect any realistic progress on them in 2024.

{kind=link}

All Comments